Last May, we shared with you why the current market is not like the last shift.

As Covid ramped up last March, many involved in the residential housing industry feared the market would be crushed under the pressure of a once-in-a-lifetime pandemic. Instead, real estate had one of its best years ever. Home sales and prices were both up substantially over the year before. 2020 was so strong that many now fear the market’s exuberance mirrors that of the last housing boom and, as a result, we’re now headed for another crash.

There are many reasons, however, indicating this real estate market is still nothing like 2008. Here are five facts to show the dramatic differences.

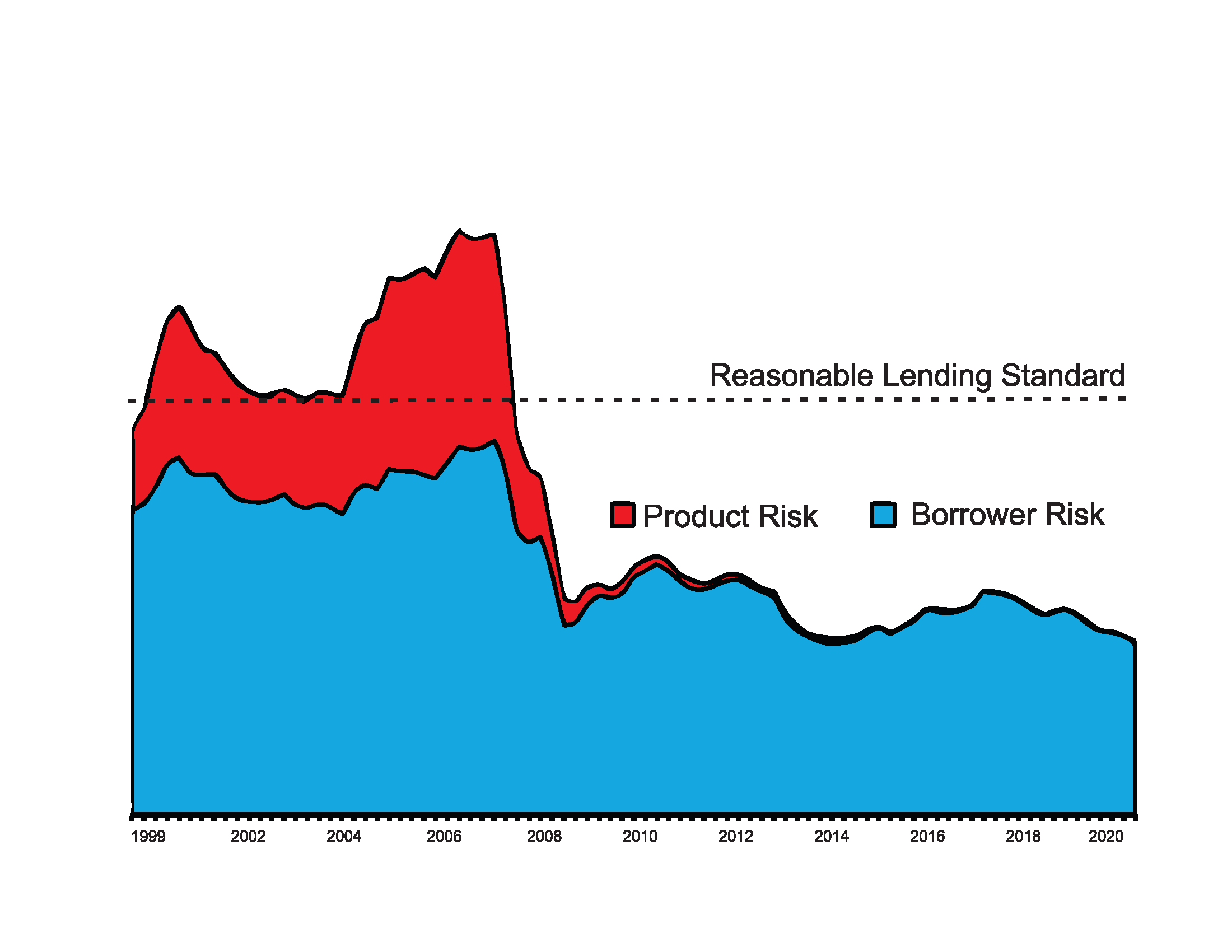

1. Mortgage standards are still nothing like they were back then.

Unlike during the last recession, the financial system is sound. During the housing bubble, it was difficult NOT to get a mortgage. Today, it is tough to qualify.

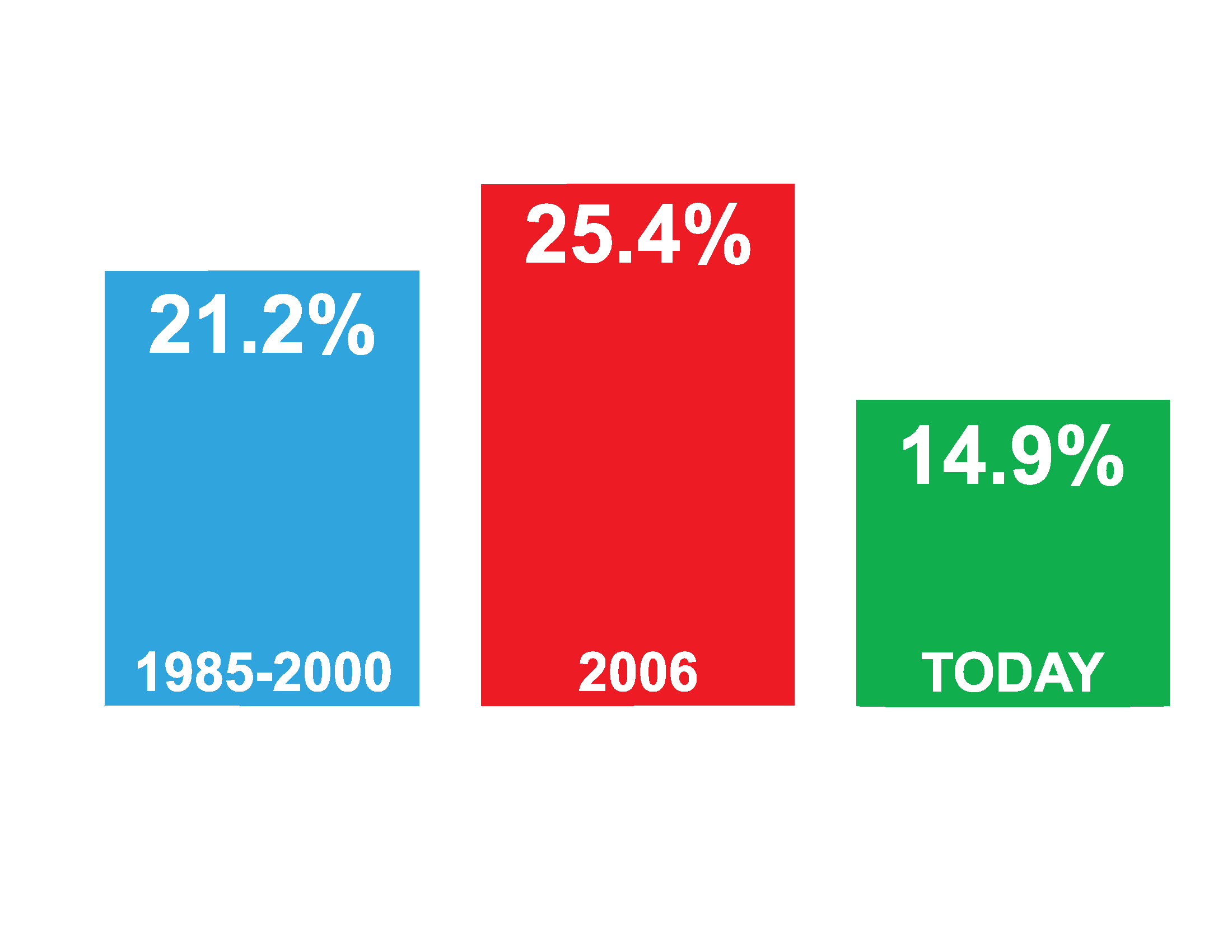

The Urban Institute releases a Mortgage Credit Availability Index which is “a summary measure which indicates the availability of mortgage credit at a point in time.” The higher the index, the easier it is to get a mortgage.

Recently, the update was released and shows that today the HCAI is under 5% which is the lowest it has been since the introduction of the index. The report notes that “if the current default risk would double across all channels, risk would still be well within the pre-crisis standard of 12.5% from 2001 to 2003 for the

whole mortgage market.”

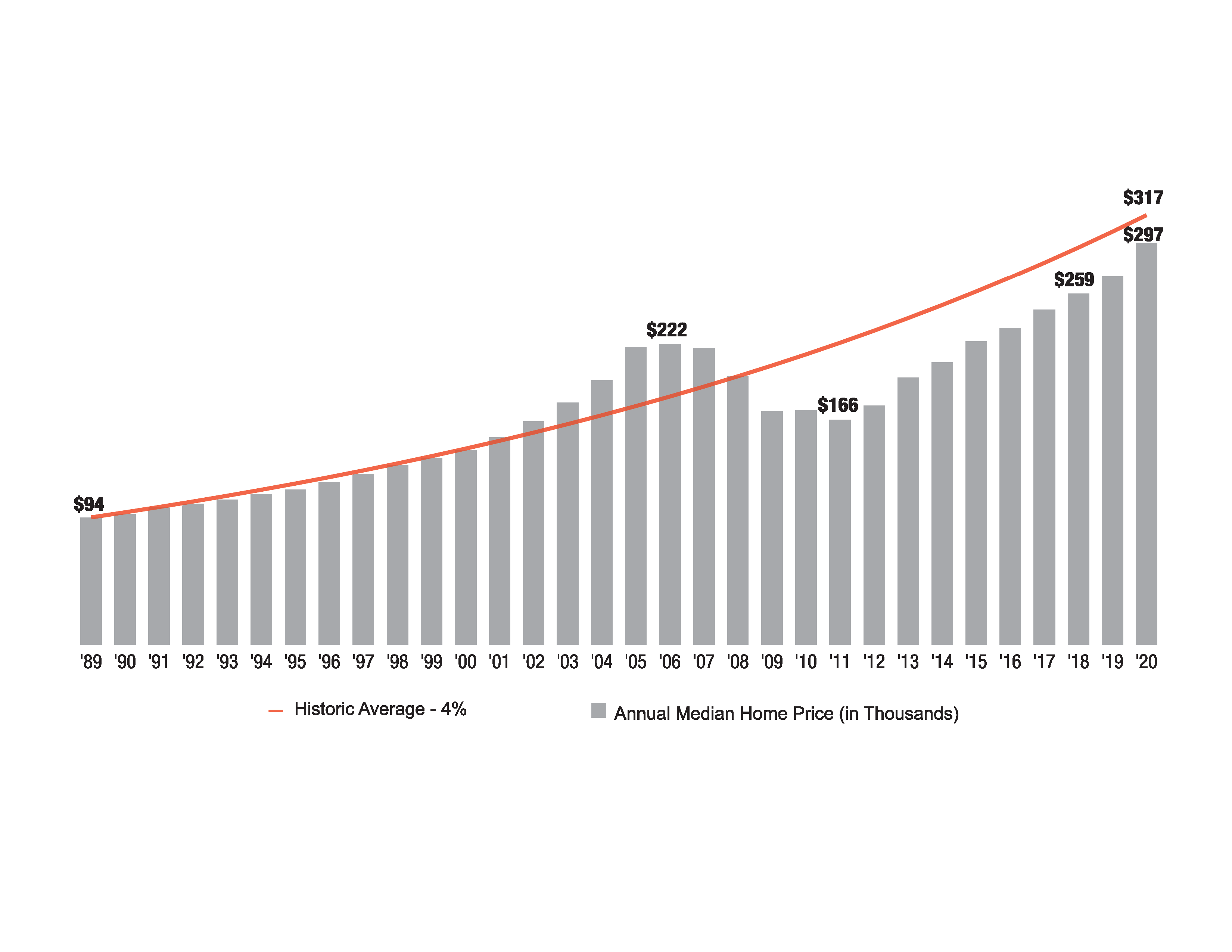

2. Despite how it feels, prices are still not soaring out of control.

Historic home appreciation is about 4%. from 2002-2005, that grew to an average of over 10% with 2004-2005 both being above 11%. 2017-2020 saw above-normal appreciation but averaged 6.25%.

As you can see on the graph, home prices are still below the 4% historic trendline as of the end of 2020.

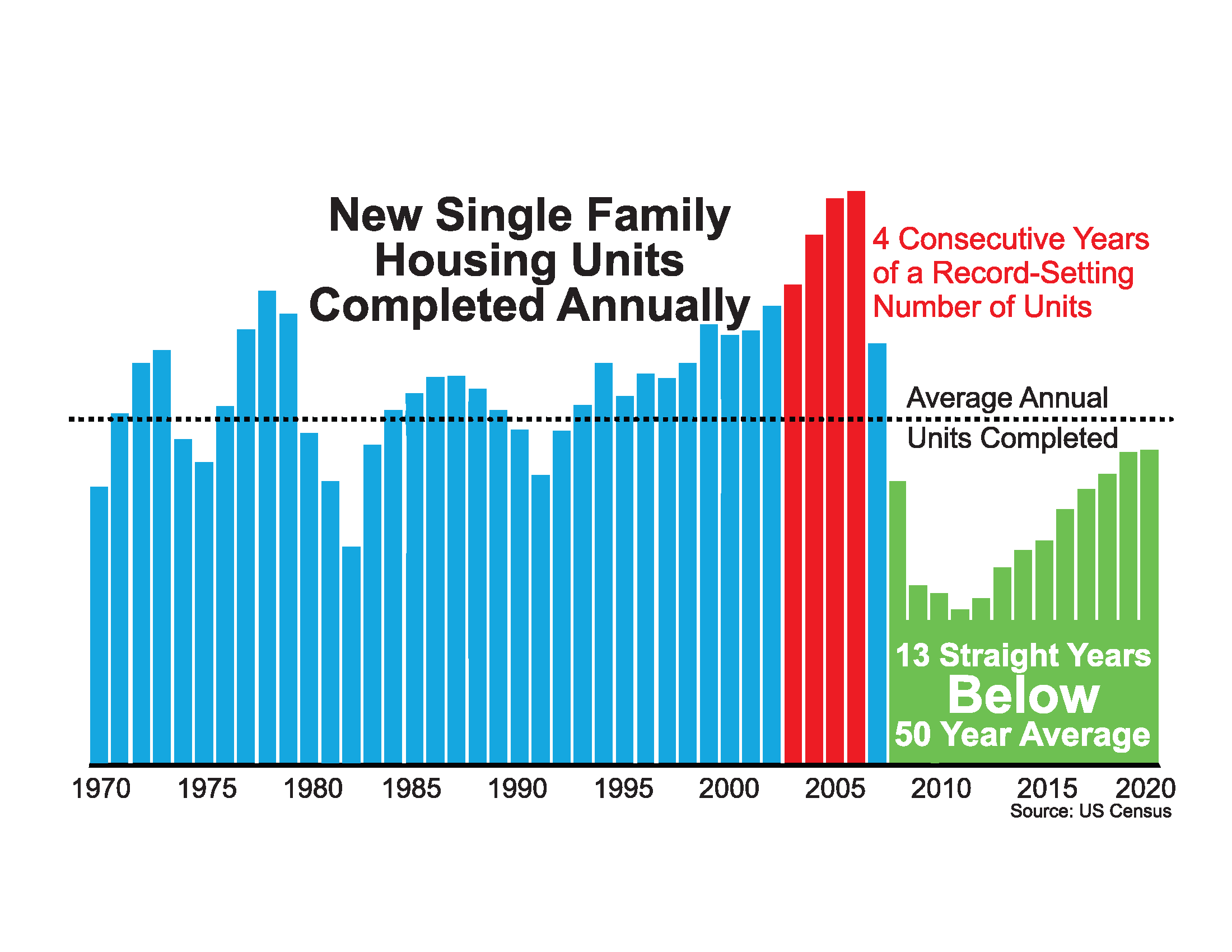

3. We still don’t have a surplus of homes on the market.

We have a shortage.

The months’ supply of inventory needed to sustain a normal real estate market is approximately six months. Anything more than that is an overabundance and will causes prices to depreciate. Anything less than that is a shortage and will lead to continued appreciation.

There were too many homes for sale in 2007, and that caused prices to tumble. Today, there’s a shortage of inventory which is causing an acceleration in home values.

Before 2007, we had four consecutive years of record-setting new home builds, resulting in an overabundance of homes. After 2007, builders slowed down significantly, and only returned to the long-term average of adding 1 million new homes each year. As a result of this 13 straight year period of being below the 50 year average, we have a significant housing shortage in America which is driving up housing prices and rents due to basic supply and demand – with fewer homes available to buy or rent, prices and rents rise.

Sellers are also more hesitant to list their homes, concerned that they may not be able to find their “next home” in a competitive market for buyers. More and more sellers are taking advantage of the Klaus Team’s Buy Then Sell program that allows homeowners to buy their next home before they sell, then list their home after they’ve moved. For more information on Buy Then Sell, visit their website at klausteam.com/buythensell.

Back in April 2005, new listings started to grow and reached epic proportions during 2006 and 2007 giving us early warning of the impending crash. 2021 has begun with the lowest inventory on record in Phoenix Metro.

4. Houses are still n/ot too expensive to buy.

The affordability formula has three components: the price of the home, the wages earned by the purchaser, and the mortgage rate available at the time.

Fifteen years ago, prices were high, wages were low, and mortgage rates were over 6%. Today, prices are still high. Wages, however, have increased and the mortgage rate is about 3%.

That means the average family pays less of their monthly income toward their mortgage payment than they did back then.

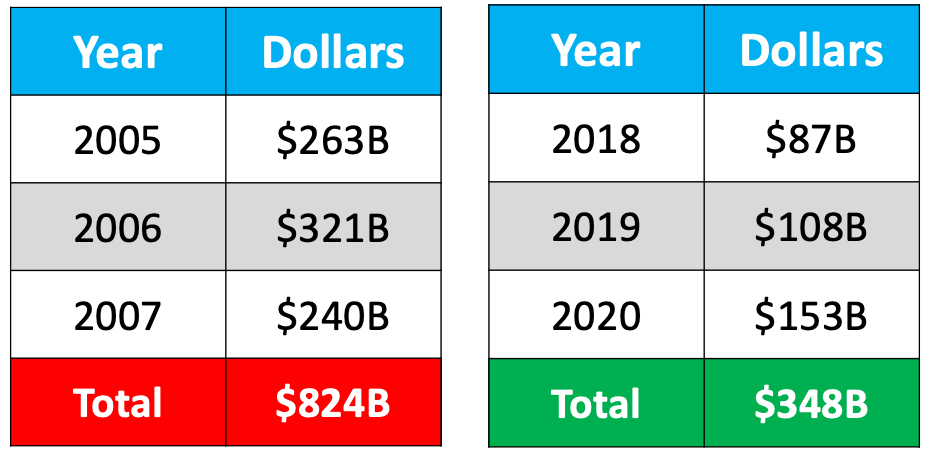

5. People are still equity rich and not tapped out.

In the run-up to the housing bubble, homeowners were using their homes as a personal ATM machine.

Prices have risen nicely over the last few years, leading to over 50% of homes in the country having greater than 50% equity. But owners have not been tapping into it like the last time.

From 2018-2020, homeowners cashed out $500 billion less than the previous period.

During the crash, home values began to fall, and sellers found themselves in a negative equity situation (where the amount of the mortgage they owed was greater than the value of their home). This caused distressed property listings (foreclosures and short sales), which sold at huge discounts, thus lowering the value of other homes in the area. With the average home equity now standing at over $190,000, this won’t happen today.

Bottom Line:

Things are different than last time, and we aren’t making the same mistakes that led to the housing crash. The market still has a positive outlook in one of the nation’s

most affordable and popular markets, Phoenix Metro.